Research Interests:

Household Finance and Financial Inclusion

Working Papers:

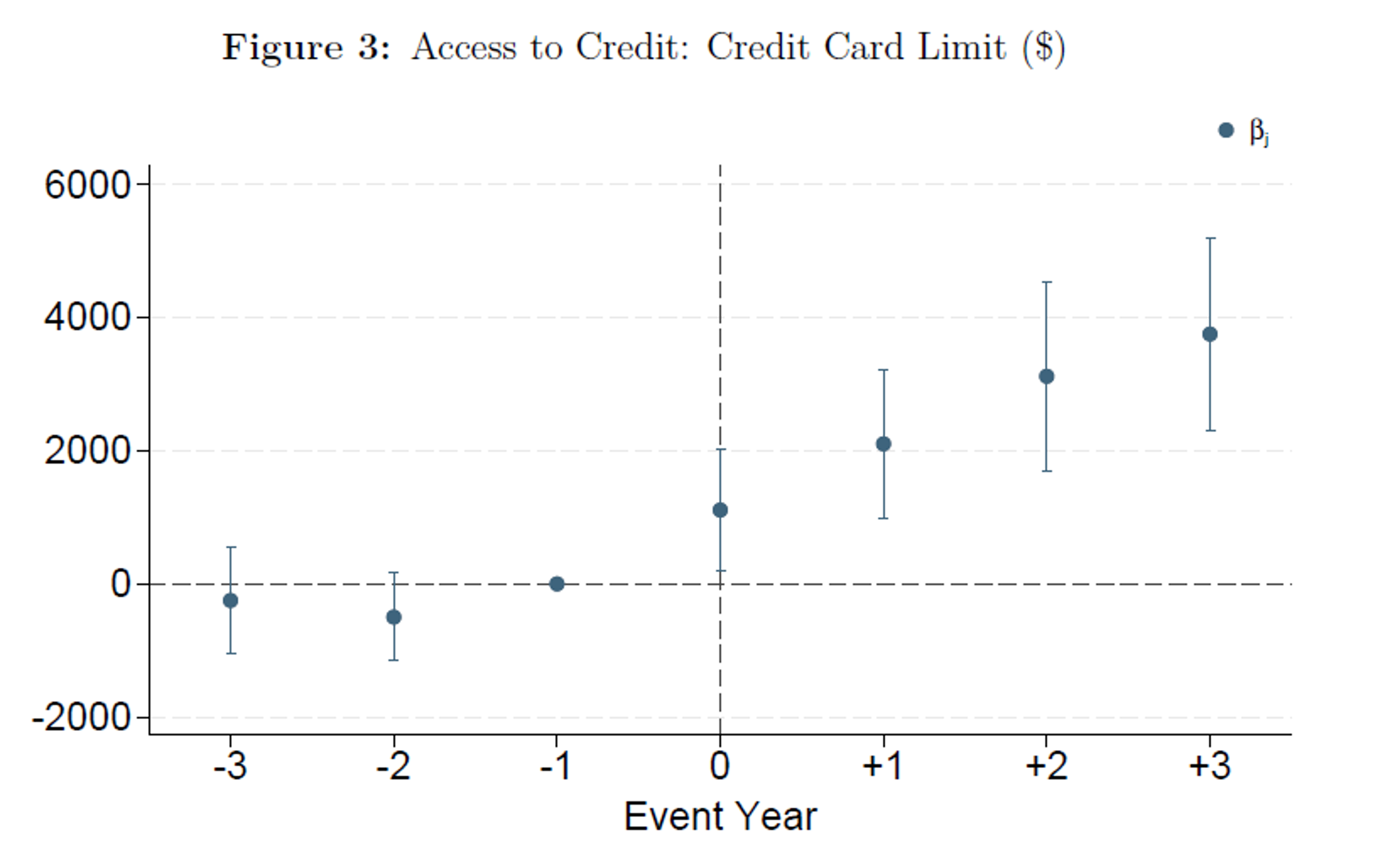

JMP House of Stolen Cards: Does Payment Security Improve Credit Outcomes for Households?

with Justin Mohr Draft

Abstract

We exploit a large-scale shift in U.S. credit card payment infrastructure to identify how payment security affects household credit outcomes. By comparing fraud-affected households to matched controls before and after the 2014 "BuySecure" initiative—which catalyzed the nationwide adoption of chip-enabled (EMV) technology—we demonstrate that while payment security restores lender willingness to lend, it fails to alleviate the demand-side scarring associated with identity theft. Using account-level credit bureau data from 2004–2020, we find that the reform led to a large and persistent decline in fraud: overall incidence fell by 70%, and repeat victimization by 61%. Lenders responded to this reduction in value-at-risk by expanding credit supply to previously fraud-exposed households, with average credit limits increasing by $3,409 (7.7%). Household responses, however, remain asymmetric; despite the improvement in security, fraud exposure continues to depress credit demand and heighten financial distress, particularly among low-score consumers. Our findings reveal that fraud is a priced lender-side risk and that payment infrastructure materially shapes credit allocation. Ultimately, while technological innovation restores lender confidence, it does not necessarily rebuild consumer trust.

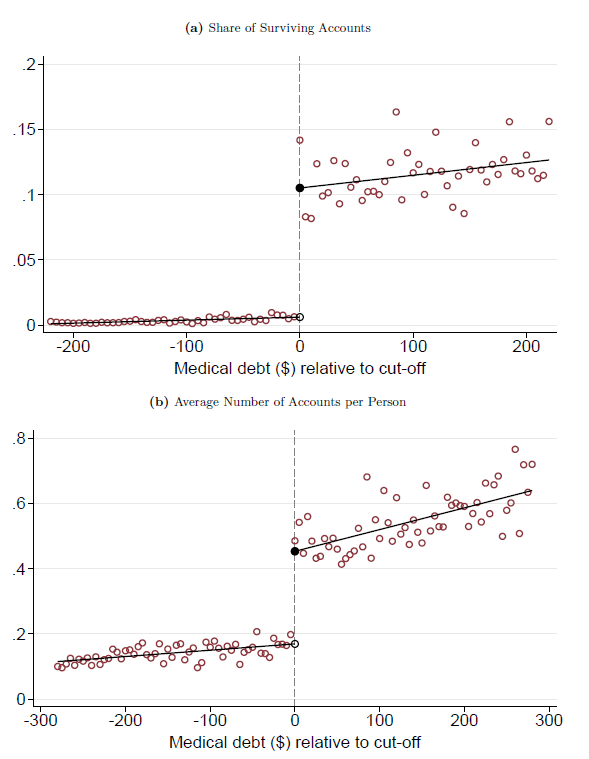

The Effects of Deleting Medical Debt from Consumer Credit Reports

with Victor Duarte, Julia Fonseca, and Julian Reif Draft

Revise & Resubmit, Journal of Finance

Abstract

In April 2023, credit bureaus stopped reporting medical debt collections below \$500. We study the effects of this information deletion on credit access and financial health. Regression discontinuity estimates comparing individuals just above and below the \$500 threshold show that deletion reduced reported medical collections by 61 percent. We find no evidence of benefits over the subsequent two years. To interpret these findings, we build credit scoring models and show that medical debts, regardless of size, add minimal information for default prediction. Our results suggest that eliminating medical collections entirely from credit reports would be unlikely to affect credit outcomes.

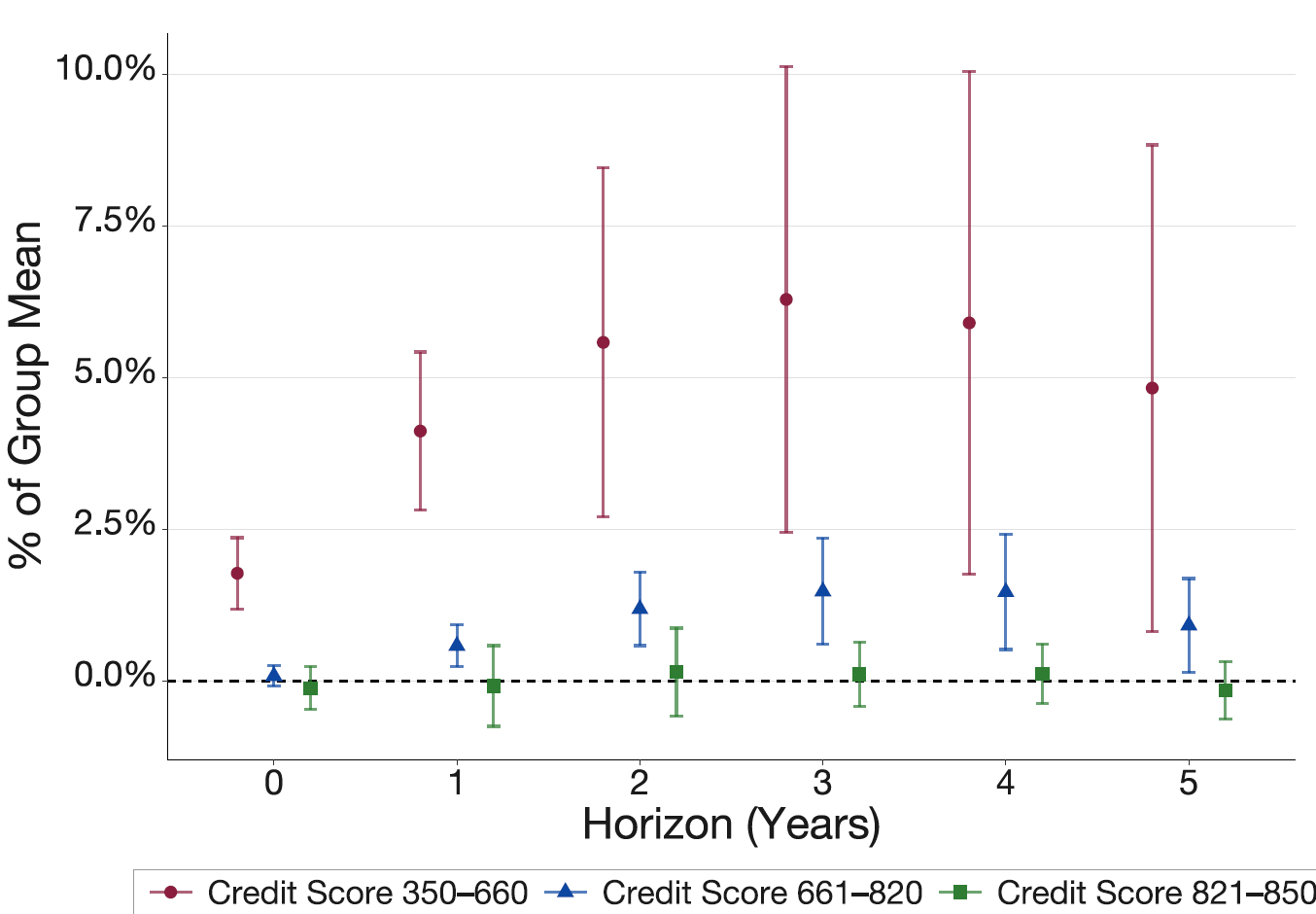

Rates Up, Balances Up: Uneven Monetary Transmission in Consumer Credit Markets

with Viraj R. Chordiya, Justin Mohr, and Yucheng Zhou Draft Additional Graphs

Abstract

What happens to consumer borrowing when interest rates rise? Standard intuition suggests that higher rates reduce borrowing by raising borrowing costs and tightening cash flow. We show that, over medium horizons, the opposite can occur. Using a representative panel of consumer credit records, we estimate dynamic responses of household debt. A 25 basis point increase in the 1-year rate raises total consumer debt by about 2% over three years ($1,539). These effects are highly uneven across households. Debt increases are concentrated among financially constrained borrowers, while high-credit-score consumers show little to no response. Additional evidence is consistent with an indirect channel: monetary tightening weakens labor-market income, and more exposed households respond by relying more on credit. Our results show that contractionary monetary policy can increase indebtedness among vulnerable households, highlighting an important distributional dimension of monetary transmission.

Work in Progress:

The Value of Protection: Domestic Violence Intervention Courts and Women’s Financial Outcomes

with Filipe Correia and Justin Mohr