Research Interests:

Household Finance, Financial Inclusion, and Banking

Working Papers:

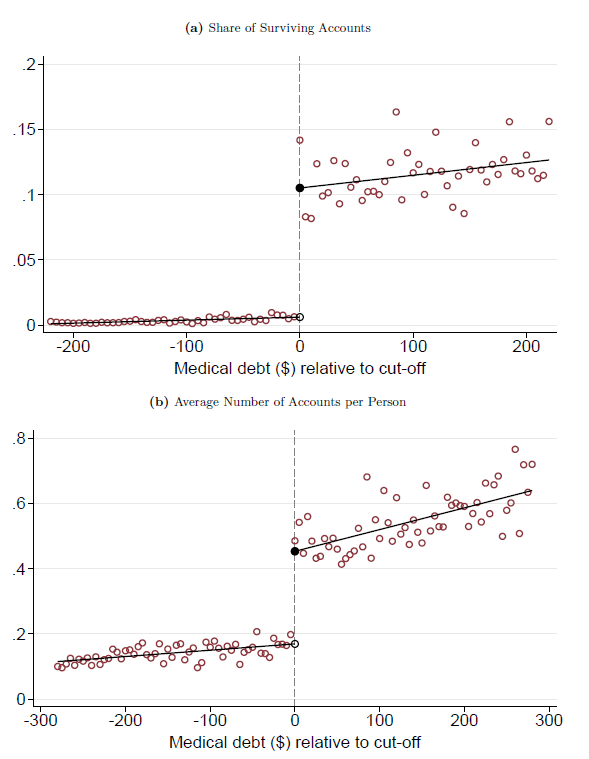

The Effects of Deleting Medical Debt from Consumer Credit Reports

with Victor Duarte, Julia Fonseca, and Julian Rief (Draft)

Abstract

One in seven Americans carry medical debt, with \$69 billion reported on consumer credit reports. In April 2023, the three major credit bureaus stopped reporting medical debt collections below $500. We study the effects of this information deletion on consumer credit scores, credit access, repayment behavior, and payday borrowing. Regression discontinuity estimates comparing individuals just above and below the \$500 threshold show that the deletion reduced the reported number of medical debt collections by 61 percent. Despite expectations that removing negative credit information would improve credit outcomes for affected individuals, we find no evidence of benefits over the subsequent two years, ruling out even small effects. To interpret these findings, we build credit scoring models and show that medical debts, regardless of size, add minimal incremental information for default prediction beyond standard credit report variables, implying that they contribute negligibly to credit risk assessment. Our results suggest that eliminating medical debt collections entirely from credit reports would be unlikely to affect credit outcomes.

Presented at: University of Illinois at Urbana-Champaign, Georgetown McDonough (coauthor)

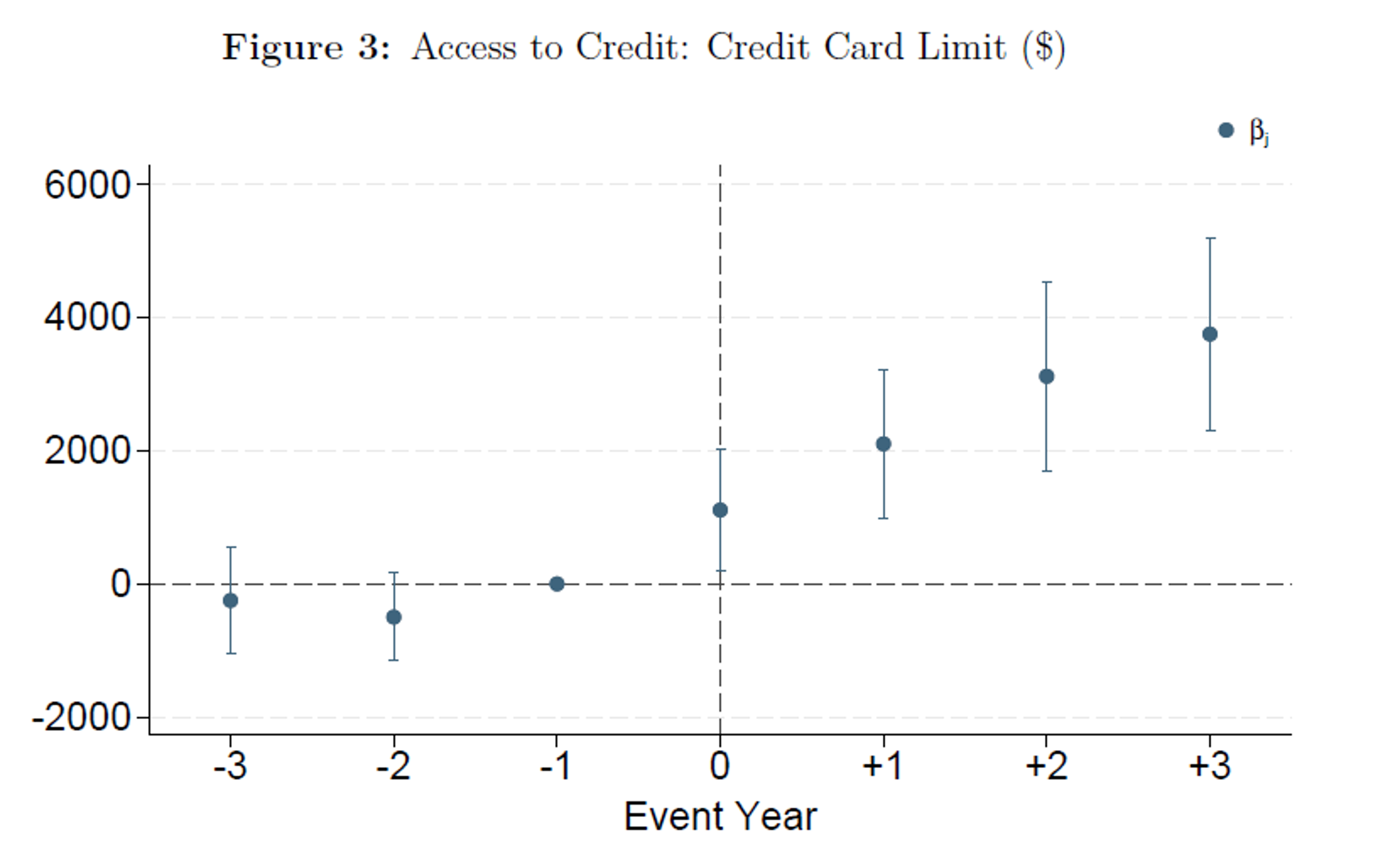

House of Stolen Cards: Does Payment Security Improve Credit Outcomes for Households?

with Justin Mohr (Draft)

Abstract

We examine how payment security shapes consumer credit markets by altering lenders’ exposure to fraud risk. Using account-level credit bureau data from 2004–2020, we exploit the 2014 BuySecure initiative—which catalyzed the nationwide adoption of chip-enabled (EMV) credit cards in the United States—as a natural experiment that sharply reduced both the probability of card-present fraud and lenders’ liability for it. We identify consumers who experience credit card fraud and construct a matched control group of observably similar individuals. The reform led to a large and persistent decline in fraud: overall incidence fell by roughly 65 percent, and repeat victimization collapsed. Lenders responded by expanding credit to fraud-exposed households, with average credit limits rising by more than \$3,000 (about 7.5 percent). Payment security thus operates as a supply-side shock, lowering lenders’ value-at-risk from fraud and restoring willingness to extend unsecured credit. Household responses, however, are asymmetric: fraud exposure continues to depress credit demand and heighten financial distress, particularly among low credit score consumers. These findings reveal that fraud is a priced lender-side risk and that payment infrastructure materially shapes credit allocation. While security innovation restores lender confidence, it does not rebuild consumer trust.

Presented at: Financial Management Association 2024 (coauthor), University of Illinois at Urbana-Champaign

Works in Progress:

The Other Half: Monetary Policy Transmission for Households without Mortgages

with Viraj Chordia, Justin Mohr and Yucheng Zhou

Presented at: Financial Management Association Early Ideas 2024